March 10, 2026

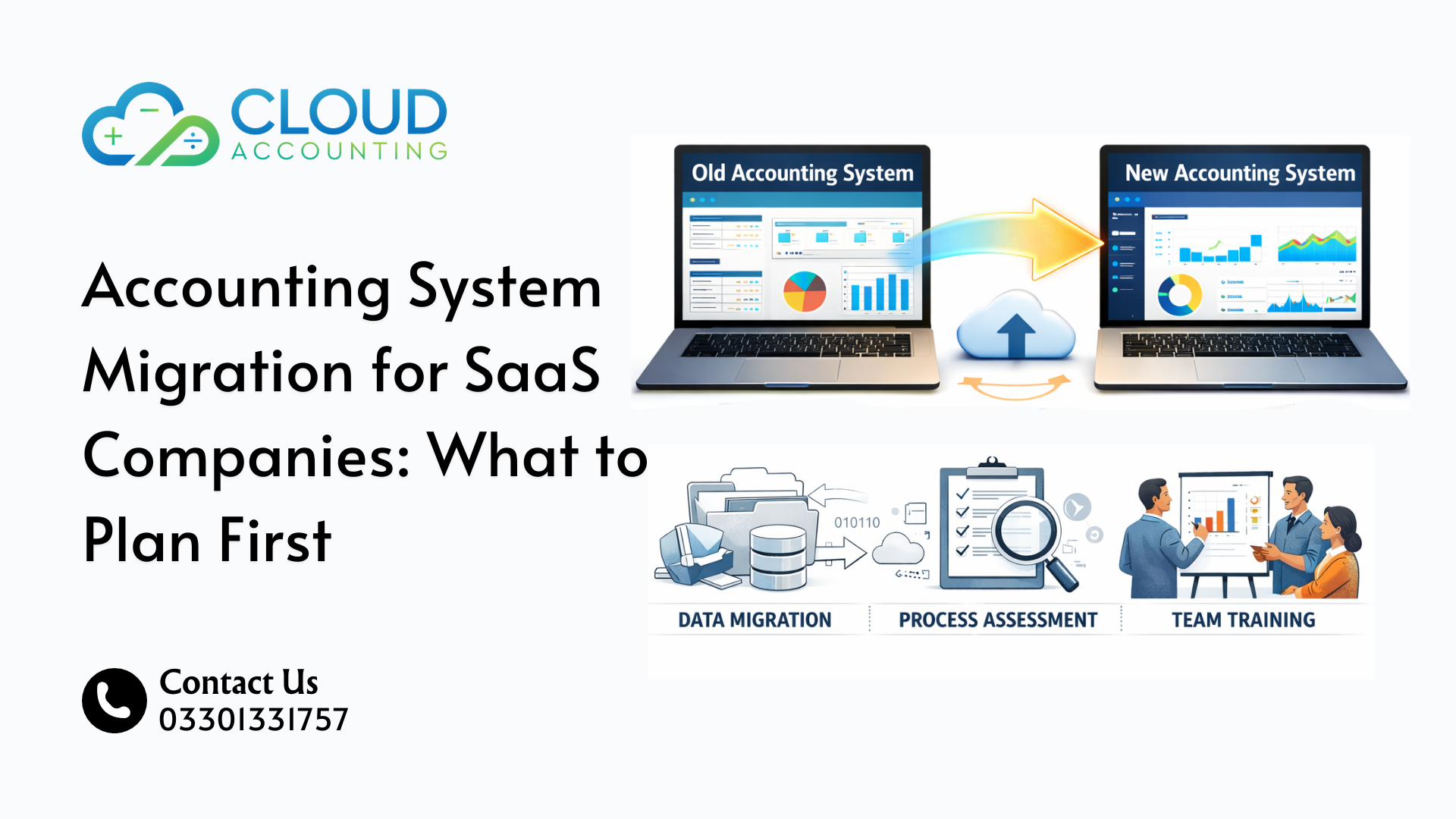

Switching to a new accounting system is a big step for any business. For SaaS companies, the process is even...

Switching to a new accounting system is a big step for any business. For SaaS companies, the process is even...

Growth in ecommerce feels exciting at first. Orders increase. Revenue climbs. New sales channels open up. Customer acquisition improves. Marketing...

Growth feels exciting at first. Revenue climbs. Customers increase. The team expands. Everything looks positive. Cash flow improves, new opportunities...

When a business is small, basic accounting tools usually feel more than enough. Invoices are sent without delay, expenses are...

Most businesses do not plan to change their accounting system. They continue using what feels familiar, even when it starts...

Excel to Cloud Accounting is not about following trends or upgrading tools for the sake of it. It is about...

A QuickBooks to NetSuite migration rarely starts because a business wants new software. Instead, it begins when the current system...

ERP projects rarely fail in a dramatic way. Most fail quietly. The system goes live, teams begin using it, and...

Most teams feel relief once NetSuite goes live. Users are active, transactions are flowing, and reports are available. On the...